Three-day delays for a simple policy change are still common for property and casualty (P&C) insurers. Manual data entry across disconnected systems creates bottlenecks that stall productivity and frustrate customers. In many cases, outdated policy administration systems require underwriters and claims teams to reconcile data manually, resulting in costly inefficiencies.

According to Lumenalta, insurers running legacy systems experience processing delays of up to three to five days for standard policy updates, and modernization can reduce those times by more than 50%. That operational drag adds up quickly for mid-sized carriers that are already spending millions on maintenance instead of innovation. According to a 2025 survey, 77.1% of carriers plan to modernize claims systems, and 73.3% are upgrading policy administration tools, highlighting the strategic urgency of transformation.

For CIOs, the challenge is people-centric: agents and underwriters need contextual, in-the-flow guidance, not static SOPs or quarterly training sessions, on utilizing new core insurance systems and new operational processes. To unlock the full value of modernization, insurers must combine next-gen core systems with people-centered enablement and digital adoption platforms.

In this article, we’ll explore what core system modernization really means for P&C insurers, why it’s essential for growth and scalability, common risks to avoid, and how Whatfix helps insurers bridge the adoption gap to drive measurable ROI.

Defining Core System Modernization in P&C Insurance

Core system modernization in P&C insurance involves a comprehensive transformation of how insurers manage claims and policy lifecycles, enabling faster processing, higher accuracy, and enhanced customer and agent experiences.

- Core System Modernization: Leading carriers are replacing outdated legacy systems with modern platforms like Guidewire and Duck Creek. These solutions offer modular, cloud-native architectures that enhance scalability, expedite release cycles, and simplify integration with other digital tools and ecosystems.

- Transforming Key Operational Workflows: Modernization redefines how insurers handle core operations across the value chain. Straight-through claims processing and automated triage eliminate manual handoffs and accelerate resolution times. Digital FNOL (First Notice of Loss) and omnichannel servicing allow customers to file and track claims from any device or channel. Streamlined policy issuance, renewals, and endorsements replace batch updates with real-time transactions, creating faster, more accurate customer experiences.

- Customer-Facing Digital Experiences: Modern platforms extend beyond back-end efficiency. They enable user-friendly web and mobile portals where policyholders can file claims, update coverage, and access documents without contacting an agent.

- Cloud-Based, API-Driven Architectures: Cloud infrastructure gives insurers the flexibility and resilience needed to scale efficiently. API-first design supports easy integration with CRMs, billing systems, and third-party data providers while minimizing technical debt and upgrade complexity.

- AI and Advanced Analytics: AI and analytics have become critical to modern insurance operations. They power predictive underwriting, automate fraud detection, and enhance decision-making accuracy across claims and policy workflows. According to Gitnux, 65% of commercial insurers now use AI to streamline claims processing, reducing cycle times by up to 50%. With a unified, cloud-based data architecture, insurers can embed these capabilities directly into their core platforms, turning every process into a source of intelligence, efficiency, and speed.

Why Should P&C Insurers Upgrade Claims & Policy Admin Systems?

Carriers stuck on legacy systems face slow processes, rising costs, and an inability to scale. Modern platforms unlock new operational capabilities and competitive differentiation.

- Accelerate Claims and Policy Cycle Times: Automating low-value tasks and reducing human handoffs can reduce claim and policy servicing times from days to minutes, providing insurers with faster turnaround and a better customer experience.

- Scalability to Handle Claim Surges: Catastrophic events can overwhelm traditional systems, underscoring the need for robust solutions. Cloud-native platforms scale elastically to absorb spikes in volume. Intelligent routing and automation enable high-volume, low-complexity claims to be processed without manual intervention, thereby preserving performance under stress.

- Enable Digital Self-Service: 79% of insurance consumers prefer digital self-service over traditional channels. That demand makes it essential for insurers to support omnichannel, mobile-friendly interfaces.

- Empower Agents and Adjusters: Frontline staff need contextual help, automation, and decision support built into their workflows. Without that, productivity, accuracy, and adoption suffer.

- Unlock AI’s Potential: A unified, cloud-based data architecture allows integration of AI and analytics to drive underwriting, fraud detection, and automated claims decisions.

- Enhance Regulatory Agility: Policy systems that support modular updates and workflow automation enable faster and less risky adaptation to regulatory changes.

- Lower Operating Costs: Reducing the burden of legacy maintenance, patching, and integration frees up IT budgets for innovation rather than endless upkeep.

- Enhance Collaboration Across the Value Chain: Connecting claims, policy, billing, CRM, and partner systems allows seamless data flow among agents, underwriters, vendors, and policyholders.

The Risks of Claims & Policy System Modernization Projects

Modernization offers huge upside, but the downside of execution failures is real. CIOs must understand and mitigate these risks.

- Underestimating IT Project Complexity of Legacy Architectures: Legacy systems often conceal tangled custom logic, hidden dependencies, and deprecated integrations. One modernization case described by BCG involved a claims-platform project that finished 50% over budget.

- Misalignment Between Business and IT Execution: When priorities diverge—business pressing for new features, while IT focuses on stability and refactoring—scope creep and rework can derail progress. In digital transformations generally, up to 70% of initiatives fail to hit objectives.

- Data Migration and Quality Issues: Migrating decades of policy, claims, and customer data is a complex and challenging task. Poor data quality, schema mismatches, and format conversions often lead to lost records or manual reconciliation. Gartner estimates that 85% of big data projects fail due to technical and governance problems.

- Change Management Risks and Downtime: Full cutovers can trigger outages and business disruption if fallback plans are weak. Delays or failures in system handover may cause lapses in customer service or compliance exposure.

- User Onboarding and Agent Training Challenges: Agents, adjusters, underwriters, and policyholders must adapt to new workflows. If training is late or disconnected from real workflows, adoption will lag, and productivity will suffer. In failed digital transformations, a common root cause is underinvested user enablement.

- Governing Usage and Preventing Workarounds: Even in modern systems, users may revert to legacy shortcuts or manual workarounds if governance isn’t enforced. Without usage controls and monitoring, system integrity and compliance will degrade.

- Tracking ROI Post Implementation: Many modernization efforts don’t define success metrics or track adoption. Without real-time analytics and governance, you can’t prove value, pivot where needed, or hold teams accountable for outcomes.

How to Realize P&C Core System Modernization ROI by Taking a People-Centered Approach with Whatfix

For CIOs leading large-scale modernization programs on platforms like Guidewire or Duck Creek, success isn’t measured by go-live dates. It’s measured by adoption. Even the most advanced system won’t deliver ROI if agents, adjusters, or underwriters can’t use it confidently and consistently.

A people-centered approach ensures that modernization investments translate into measurable outcomes. Whatfix for P&C insurers enables organizations to accelerate core system adoption and drive ROI through hands-on learning, in-app guidance, just-in-time support, and continuous analytics, empowering employees to master new systems through guided workflows and contextual experiences.

Here’s how Whatfix redefines technology by enabling users:

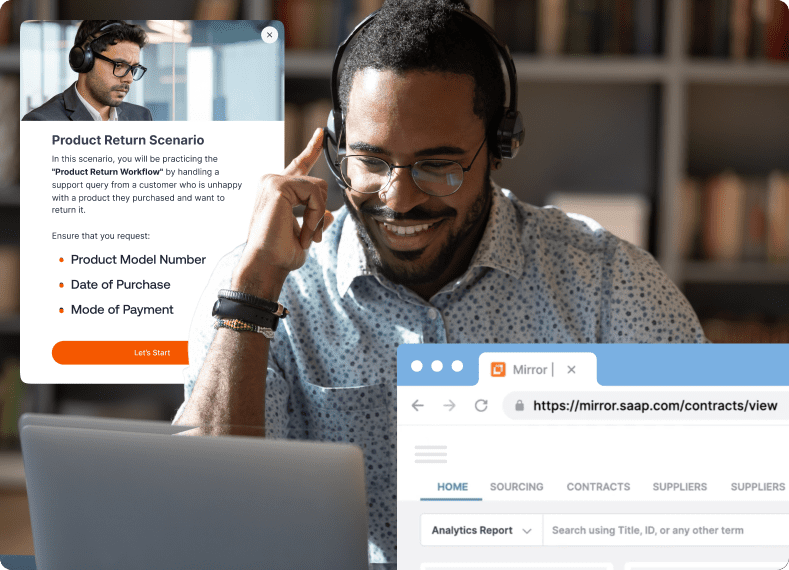

1. Simulated Claims and Policy Workflow Training

Traditional training models can’t keep up with the pace and complexity of modernization. Whatfix Mirror enables insurers to create interactive simulations that mirror live claims and policy workflows before going live, providing hands-on training simulations for policy and claims agents. Agents and underwriters can practice end-to-end processes like policy issuance, renewals, or FNOL submissions in a controlled, risk-free sandbox environment. These simulations help users gain hands-on experience, identify pain points early, and build confidence ahead of deployment.

By tracking completion times and error rates during simulated training, insurers can pinpoint where users struggle and refine both training and process design. This leads to faster proficiency and fewer post-launch support issues once the system goes live.

2. AI Roleplay and Scenario Training

P&C operations are unpredictable. Whatfix Mirror’s AI roleplay allows insurers to recreate realistic claims and policy scenarios for training at scale. Adjusters can practice managing high-volume catastrophe claims, learning how to triage, prioritize, and document efficiently under pressure. Underwriters can run simulated pricing or policy adjustments that reflect current rules and regulatory updates.

These scenario-based experiences build operational readiness for complex situations and reduce the learning gap between training and live production. The result is higher accuracy, faster decisions, and improved performance across teams.

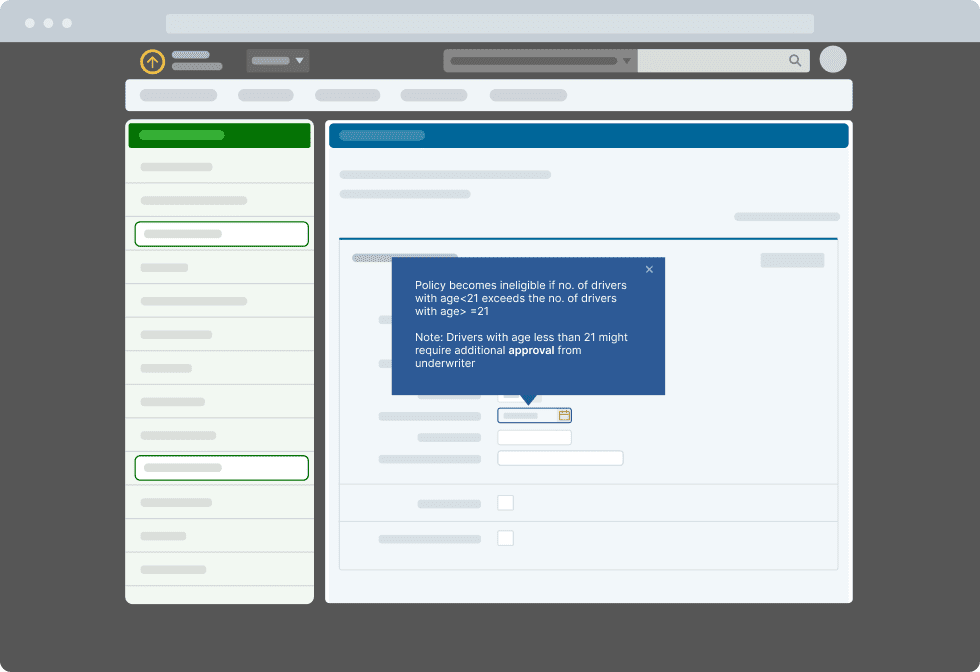

3. In-App Guidance in the Flow of Work

Once a system is live, employees shouldn’t have to leave their workflow to find help. Whatfix Digital Adoption Platform (DAP) provides step-by-step, in-app guidance that appears directly within platforms like Guidewire, Duck Creek, or Majesco.

If a claims adjuster needs to process a multi-claim submission, Whatfix displays the exact sequence of actions to complete the task correctly. Contextual tips, interactive walkthroughs, and prompts guide users through complex workflows in real time. This reduces dependency on external documentation, eliminates guesswork, and standardizes processes across the organization. It also helps global teams maintain consistency and compliance while accelerating time to productivity.

With Whatfix’s AI Agents, digital leaders and L&D teams can put AI to work by automating the creation of in-app content and guided workflows to deliver contextual, AI-powered support directly in the flow of work.

4. Embedded Self-Service Help

Insurers often maintain large repositories of training documents and SOPs that employees rarely access when they need them most. Whatfix transforms these static resources into embedded, searchable help that resides directly within the system.

Agents and adjusters can find answers, videos, or articles relevant to their specific task without leaving the page. The Whatfix Self Help widget connects to existing knowledge bases, LMS content, or intranet resources to deliver information in the flow of work. End-users can use AI conversational search to ask for contextual help, summarize documents, and quickly find the enablement resources and process documentation at the moment of need.

This approach reduces help desk tickets, accelerates problem resolution, and keeps users productive during high-volume periods. It also ensures that learning and support resources evolve in parallel with system updates.

5. AI-Powered Enablement

Core insurance systems can only deliver full value realization when employees use them effectively. Whatfix drives ROI by embedding AI-powered assistance directly into these systems, enabling insurers to modernize their workforce’s learning, execution, and optimization of work.

Whatfix integrates AI across its platform to deliver contextual, just-in-time enablement within daily workflows. This ensures that every underwriter, claims adjuster, and operations analyst receives personalized support tailored to their role, behavior, and process stage, all without leaving the application. This includes capabilities like:

- Authoring & Guidance Agents automatically update in-app Flows, Smart Tips, and contextual guidance as processes evolve. They analyze user role, behavior, and input to dynamically generate or refine content, ensuring that every workflow reflects the latest business logic and compliance standards.

- AI Insights proactively identifies friction points, inefficiencies, and adoption gaps in core insurance systems. It surfaces these insights to application owners and business process leaders, working in tandem with the Guidance Agent to auto-launch new in-app experiences or nudges that address those issues before they impact KPIs.

- AI Roleplay creates interactive, scenario-based simulations for claims and underwriting teams. These roleplays replicate real-life decision-making and system navigation, enabling employees to practice judgment calls and process execution in a safe environment that accelerates competency and confidence.

- QuickRead uses AI to summarize complex policy, claims, or regulatory documentation within the application, allowing adjusters and underwriters to access the key information they need instantly while maintaining compliance accuracy.

- AI in Self Help delivers hyper-contextual, conversational support. It interprets user queries, pulls answers from enterprise knowledge bases, and dynamically ranks results based on context, intent, and prior behavior, thereby reducing dependency on service desks and improving first-contact resolution rates.

Whatfix’s AI capabilities close the gap between digital transformation intent and actual value realization by turning every user interaction within core systems into an opportunity for enablement, optimization, and insight. For P&C insurers, use cases include:

- Claims Intake and Validation: AI-guided workflows ensure agents capture required data fields correctly, reducing rework and processing delays.

- Fraud Detection Alerts: AI Insights identifies abnormal claim patterns and surfaces process guidance to prompt additional verification steps.

- Underwriting Risk Assessment: Guidance Agents tailor step-by-step instructions based on policy type, coverage, and regulatory requirements.

- Claims Adjudication Training: AI Roleplay replicates adjudication decisions for hands-on, adaptive training.

- Policy Review and Approval: QuickRead condenses complex policy or coverage documentation for faster, more accurate approvals.

- Knowledge Retrieval: AI in Self Help provides contextual knowledge when underwriters or adjusters search for process clarifications or compliance rules.

6. Track Adoption, Optimize Workflows, and Prove ROI

Once modernization is complete, tracking ROI becomes the next challenge. Whatfix Analytics provides full visibility into how users engage with systems, where inefficiencies exist, and which processes need attention.

Dashboards display usage rates, completion times, and productivity metrics across regions or departments. CIOs can correlate adoption data with business KPIs such as reduced claims cycle time, improved policy accuracy, or decreased training costs.

This data closes the loop between technology investment and measurable business value. It allows insurers to continuously optimize workflows, improve user experiences, and demonstrate quantifiable ROI to executive stakeholders.

Core Metrics to Track:

- Claims processing time and settlement accuracy

- Policy administration efficiency and SLA compliance

- Adoption rate, proficiency, and time-to-proficiency

Continuous Optimization Through Analytics:

- Using DAP data to identify friction in workflows

- Refining processes based on real-time user behavior

- Ensuring modernization evolves with business goals

P&C Core System Modernization Clicks With Whatfix

Modernization in P&C insurance isn’t just a technology upgrade. It’s the foundation for operational agility, regulatory resilience, and lasting customer trust. Replacing legacy systems with modern platforms, such as Guidewire or Duck Creek, unlocks enormous potential. However, the fundamental transformation occurs when people adopt these systems with confidence and consistency.

Insurers that combine modernization with digital adoption realize faster ROI, stronger collaboration, and better customer outcomes. They turn complexity into capability and ensure every agent, adjuster, and underwriter has the tools and knowledge to perform at their best.

How Whatfix Enables Modernization Success:

- Accelerates employee proficiency on new claims and policy systems

- Reduces training time, support tickets, and change management friction

- Ensures compliance and consistency through guided workflows

- Delivers adoption analytics to measure ROI and optimize performance

Whatfix helps leading P&C insurers transform modernization from a technology project into a measurable business advantage.

Explore how Whatfix for P&C insurers enables organizations to modernize claims and policy systems to accelerate adoption and ROI. Request a demo now.