Core banking systems, the centralized platforms that manage daily transactions, accounts, and lending, were built for reliability rather than agility. Most are decades old, relying on monolithic architectures and batch processing that can’t support open APIs, real-time data, or the pace of digital innovation demanded today.

It’s no surprise that 55% of banks say legacy core limitations are the most significant barrier to achieving their business goals. At a time when fintechs are redefining service speed and customer experience, these constraints are becoming unsustainable.

Application modernization has become a strategic priority across the industry. Banks are rethinking their entire technology stack, from the back-end core to customer-facing channels, to deliver faster products, ensure compliance, and scale for the future. But technology alone isn’t enough.

To unlock core system ROI, banking teams need the right user enablement strategy, from hands-on training to performance support in the flow of work. Employees across branches, operations, and IT must be guided through new systems with guided support at the moment of need, AI that enables users with contextual experiences, and analytics that accelerate adoption and drive lasting productivity gains.

In this article, we’ll explore what core banking modernization really means, the business outcomes driving it, the risks that come with it, and how a people-centered adoption strategy helps banks achieve measurable transformation.

Defining Core Banking System Modernization

Core banking modernization is a complete transformation of how banks deliver, manage, and scale financial services. It replaces rigid, decades-old infrastructures with flexible, cloud-based platforms that support continuous innovation and real-time operations.

Traditional cores were built for transactional reliability, but they’ve become barriers to agility and integration. Modernization introduces a new foundation, one that connects every part of the banking ecosystem, from customer-facing channels to back-office processes, through open APIs and real-time data flows.

Core banking modernization includes:

- Modern core platform replacement or transformation, using platforms like Temenos, Finacle, FIS, or Fiserv to enable real-time data processing and extensible APIs.

- Re-engineering key banking workflows such as account management, fund transfers, loan origination, servicing, payments, reconciliation, and exception handling to operate in real time.

- Implementing digital onboarding and self-service account setup to simplify KYC processes and enhance customer experiences.

- Integrating customer-facing experiences with backend systems for a unified, omnichannel banking environment.

- Adopting cloud-native, API-driven architectures that provide scalability, interoperability, and seamless integration with fintechs, payment gateways, and partner ecosystems.

- Embedding AI and advanced analytics to drive real-time fraud detection, credit scoring, personalized recommendations, and predictive decision-making.

What’s the Difference Between Legacy & Next-Gen Core Banking Systems?

The primary differences between legacy, core, and next-generation banking systems stem from their technology architecture, flexibility, the bank’s ability to innovate with these platforms, and integration considerations.

Legacy Core Banking Systems

Legacy systems are often monolithic, having been built decades ago on mainframes and proprietary codebases, such as COBOL. They rely on batch processing, meaning transactions are executed in groups at set times rather than being processed instantly. These systems were built for stability and compliance but lack agility.

They’re difficult to update, require specialized technical expertise, and often can’t easily integrate with modern APIs, fintech applications, or real-time analytics tools. This slows down innovation, limits new product launches, and increases operational costs. Many large banks still run critical operations on these legacy cores because of the risk and cost involved in replacing them.

Traditional (Modernized) Core Banking Systems

Traditional core banking systems represent a step forward; they retain centralized architecture but are modular, allowing banks to add or upgrade components (like loans or payments) without overhauling the entire system.

These systems often support real-time processing, cloud hosting, and standardized APIs. However, while they’re more flexible than legacy systems, they’re still largely on-premises and rely on extensive customization. This can make scalability and continuous innovation challenging when compared to newer, cloud-native platforms.

Next-Generation Banking Systems

Next-generation systems are cloud-native, API-first, and built on microservices architectures. This design enables banks to scale individual services independently, deploy updates more quickly, and integrate seamlessly with fintech ecosystems.

They support real-time data streaming, AI-driven personalization, open banking compliance, and automated DevOps pipelines, enabling banks to roll out new products or digital experiences in weeks rather than months. Vendors like Thought Machine (Vault), Mambu, and Temenos Infinity are leading this shift.

Next-gen cores also enable composable banking, where banks can build and reconfigure services like Lego blocks to adapt quickly to market or regulatory changes.

Why Banks Are Modernizing Core Systems

For most banks, modernization isn’t about chasing the latest technology trend. It’s a strategic business imperative driven by the need for operational agility, faster innovation, and seamless customer experiences. As digital-first competitors and fintechs continue to raise expectations, outdated core systems are becoming the single biggest constraint on growth and efficiency.

- Accelerate Transaction and Service Speed: Cloud-native platforms enable real-time processing, eliminating delays associated with overnight batch runs. This improvement enhances both customer satisfaction and operational efficiency. According to McKinsey, banks digitizing the loan-closing and fulfillment experience would shrink wait time from days to minutes, directly impacting customer retention and service quality.

- Enable Digital Self-Service: Today’s customers expect to open accounts, transfer funds, and resolve issues instantly across mobile, web, and in-branch channels. Legacy systems often lack the API infrastructure and responsiveness to support these experiences. Modern platforms make omnichannel banking seamless, enabling customers to complete tasks without manual intervention or staff assistance.

- Empower Frontline Employees: Modern core systems improve employee productivity by unifying data and automating low-value tasks. Real-time access to customer information, account histories, and product data enables employees to make faster, data-driven decisions. Routine activities like account maintenance, payment processing, and balance reconciliation are automated, freeing staff to focus on advisory and relationship-driven work that adds more value to the customer and the business.

- Unlock AI and Data Insights: Next-generation cores consolidate structured and unstructured data across systems, creating a single source of truth for analytics and AI-driven decisions. Banks can use this unified data to improve credit risk modeling, detect fraud in real time, and deliver personalized product recommendations that increase cross-sell and upsell opportunities.

- Enhance Regulatory Agility: Compliance has always been one of banking’s most resource-intensive functions. Modern cores automate data reporting and audit workflows, reducing the time and manual effort needed to stay compliant. Real-time monitoring and documentation also help banks adapt more quickly to regulatory changes and avoid costly fines.

- Scale for Growth and Flexibility: Modern, modular architectures make it easier for banks to expand into new markets, launch digital products, or integrate with third-party fintech solutions. Open APIs allow for faster ecosystem connectivity, whether that’s with digital wallets, payment networks, or new credit scoring platforms, without heavy redevelopment or downtime.

- Lower IT and Maintenance Costs: Outdated systems require constant patching, manual updates, and expensive maintenance contracts. By reducing dependence on legacy infrastructure, banks can lower operational costs and redirect IT budgets toward innovation, analytics, and customer experience initiatives.

- Improve Collaboration Across Channels: Unified systems connect retail, commercial, and digital operations into a single environment. This eliminates data silos, enhances visibility across teams, and creates smoother collaboration between front-office staff, back-office operations, and customer support. The result is a more cohesive customer journey, from onboarding to servicing to retention.

The Risks of Core Banking System Modernization

Modernization is a high-stakes initiative that affects every part of a bank’s operations. Without careful planning and alignment, projects can stall, go over budget, or fail to deliver measurable ROI.

- Underestimating the complexity of legacy integrations and data migration: Decades of historical data, fragmented platforms, and custom-built integrations make migration one of the most challenging tasks. Poor data quality, incomplete mapping, and dependency issues can lead to costly delays and system downtime during rollout.

- Focusing on technology features instead of business impact: Many projects become entangled in achieving feature parity rather than aligning new capabilities with measurable business outcomes, such as reduced operating costs, faster product launches, or improved customer satisfaction.

- Change management challenges like service disruption and resistance to new processes: Modernization disrupts established workflows. Without proactive communication, training, and executive sponsorship, employees may resist ueadoption, and even short service interruptions can harm customer trust.

- User onboarding and training for banking staff: Frontline employees (loan officers, lenders, tellers, and support agents) need to adapt to new workflows quickly. Without proper enablement, productivity drops, error rates rise, and the customer experience suffers.

- Governing usage and driving ROI: Post-launch, banks often struggle to track adoption or measure performance. Without strong usage governance and analytics, it’s hard to identify inefficiencies or prove the ROI of modernization investments.

Strategies to De-Risk Core Banking Modernization & Realize ROI

Core banking modernization is one of the most complex and resource-intensive transformations a financial institution can undertake. Success depends not only on technology but also on how well banks prepare, train, and empower their personnel to adapt to new systems, workflows, and evolving customer expectations.

These strategies help banks reduce transformation risk, accelerate user adoption, and translate modernization investments into tangible ROI.

1. Simulation-Based Training for Hands-On Practice

Before a single workflow goes live, banks can upskill their teams through realistic digital simulations that mirror the new system’s interface and processes. Employees can safely practice essential workflows, like creating customer accounts, approving loans, processing payments, or reconciling transactions, without disrupting live systems.

This simulation-based training approach turns training into an interactive experience rather than a passive exercise. Employees gain familiarity with new layouts, navigation patterns, and compliance steps before launch, which:

- Shortens time-to-proficiency by weeks.

- Reduces early-stage user errors that often lead to compliance breaches or customer dissatisfaction.

- Helps identify process gaps or configuration issues before the platform is fully deployed.

For large retail banks rolling out modernization across multiple regions or subsidiaries, simulations also ensure standardized training that scales without requiring in-person workshops or instructor-led sessions.

Whatfix Mirror enhances this simulation-based approach by creating high-fidelity replicas of the bank’s core banking applications for hands-on learning. With Mirror, teams can train within a fully interactive, sandboxed environment that looks and behaves exactly like the live system—without any risk to real data or operations. This allows employees to practice complex workflows like loan origination, payment approvals, or compliance checks in a safe, guided setting.

Because Mirror automatically syncs with the latest system configurations, training content stays accurate even as processes or UI elements evolve. Banks can scale consistent, up-to-date simulations across regions and roles, reducing training maintenance costs while ensuring every employee gains confidence and proficiency before go-live.

2. AI-Driven Roleplay and Scenario-Based Learning

Banking operations are nuanced. Loan officers, underwriters, tellers, and compliance teams all face unique edge cases every day. Whatfix’s AI scenario training replicates those real-world challenges using contextual, adaptive simulations.

For example, an AI roleplay exercise might test a lender’s decision-making during a credit review or simulate a teller handling a complex foreign transaction. The system provides personalized feedback, scores performance, and automatically recommends targeted follow-up modules to address areas for improvement.

This approach transforms mandatory compliance and risk training into dynamic, data-driven enablement, helping banks reduce human error, maintain regulatory integrity, and boost employee confidence under pressure – all in a risk-free environment that prepares them for real-world tasks and customer interactions.

3. In-App Guidance in the Flow of Work

Once live, Whatfix Digital Adoption Platform enables learning in the flow of work. Rather than switching between systems, manuals, or help desks, employees receive contextual walkthroughs, prompts, and tooltips inside the core application.

This empowers users to complete complex tasks, like loan restructuring, customer onboarding, or fund reconciliation, without leaving their workspace or interrupting productivity. For instance:

- A loan officer processing a mortgage application receives guided steps tailored to customer type or risk profile.

- A teller handling a foreign exchange transfer is automatically prompted with current regulatory documentation or rate thresholds.

Banks can also deploy in-app guidance on customer-facing digital channels, like online or mobile banking portals. This helps customers self-serve common requests, like activating cards, adding beneficiaries, or setting up auto-pay, reducing call center volume and improving digital engagement.

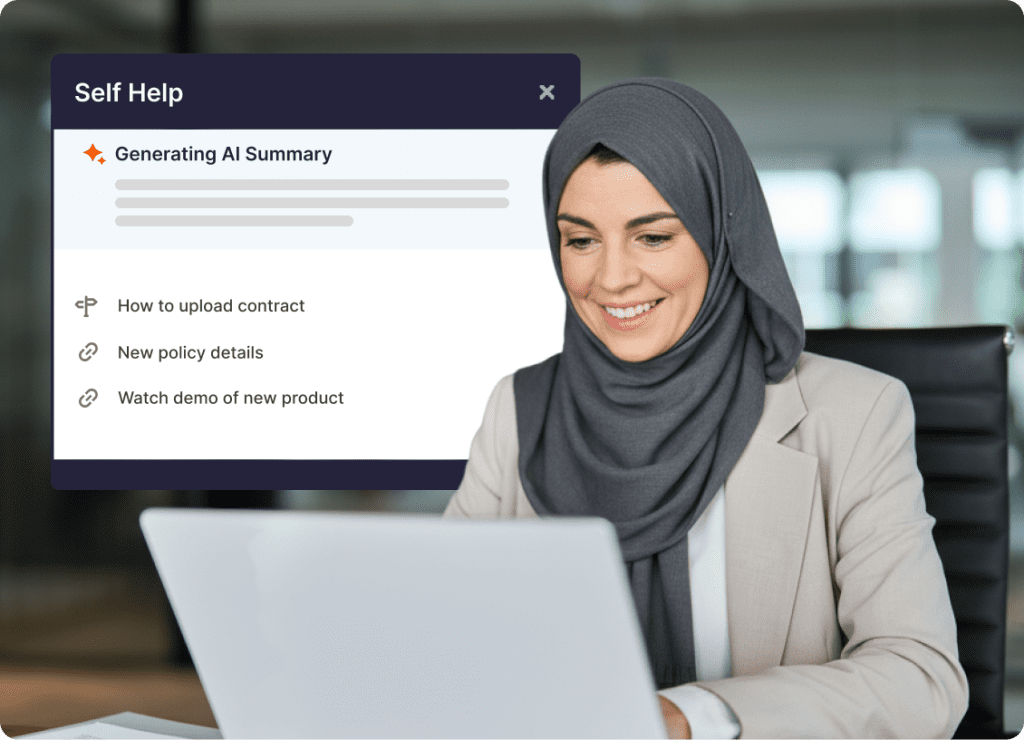

4. Embedded Self-Service Support

Whatfix transforms internal knowledge and SOPs into dynamic, AI-powered self-help directly accessible within the banking platform. Employees can search natural-language queries (“How do I reverse a transaction?” or “What’s the process for loan settlement?”) and instantly access contextual answers, videos, or guided steps.

By consolidating content from internal wikis, policy documents, and training manuals, Whatfix eliminates knowledge silos and ensures every employee gets consistent, accurate information, no matter their branch, department, or system version.

This same self-service capability can be extended to customers. For example, an accountholder using the digital portal can ask “How do I dispute a charge?” and receive instant AI-guided steps to complete the process. For the bank, this means fewer support tickets, lower operational costs, and improved customer satisfaction.

5. AI-Powered Enablement

Whatfix doesn’t just guide, it automates. Through AI-powered intent detection, the platform recognizes user behavior and proactively surfaces the next-best action, ensuring employees follow the right process every time.

For example:

- When a user begins verifying a customer’s identity or checking a transaction status, Whatfix automatically prompts the correct sequence of steps and validation checks to ensure accuracy.

- If the transaction is marked as disputed, the system guides the employee through explaining fraud protection policies, blocking the compromised card, and initiating a replacement.

- As the workflow concludes, Whatfix ensures the user records the fraud cause for investigation and compliance documentation, preventing skipped steps or incomplete case logs.

These micro-automations create built-in safeguards for accuracy, compliance, and performance, key pillars of any successful modernization program. Over time, Whatfix analytics learn from user behavior to predict where friction will occur and proactively eliminate it.

6. Track Adoption, Optimize Workflows, and Prove ROI

Modernization ROI depends on one key factor: how effectively employees utilize the system. Whatfix analytics give banks deep visibility into user adoption, process completion rates, and feature utilization.

With these insights, banks can:

- Identify where employees struggle or abandon workflows.

- Measure how long it takes for staff to reach proficiency.

- Quantify productivity gains, error reductions, and compliance adherence.

Leadership teams gain a clear, data-backed view of modernization success, while IT and operations teams can continuously refine user journeys, retrain employees as needed, and eliminate workflow bottlenecks that slow the realization of value.

IT and L&D leaders are commercial banks and financial service institutions should look at the following metrics to track to understand core banking system modernization adoption:

- Account setup and transaction processing times

- Loan and payment servicing SLAs

- Employee proficiency and adoption rates

- Error reduction and compliance adherence

- Support ticket volume and time-to-resolution

Whatfix Product Analytics gives banking leaders a complete, data-driven view of how employees interact with new core systems. It visualizes real user behavior to uncover friction points, workflow drop-offs, and efficiency gaps across roles, branches, or regions. With these insights, banks can continuously refine training and in-app guidance to address the exact challenges employees face in the flow of work.

By linking behavioral data to key metrics—like process completion time, adoption rate, and compliance accuracy—Product Analytics helps teams measure the tangible impact of modernization initiatives. This enables continuous optimization of workflows and ensures modernization success scales as business needs evolve.

Banking Modernization Clicks Better with Whatfix

Modernization isn’t just about upgrading technology. It’s about transforming how banks operate, innovate, and build trust with their customers. A new core platform provides the digital foundation, but it’s the people and processes around that technology that ultimately determine success.

Banks that combine modernization with a strong digital adoption strategy achieve faster ROI, higher productivity, and sustainable competitive advantage. By empowering employees with contextual guidance, AI-driven training, and continuous feedback, they unlock the full potential of their investment and drive long-term transformation across the enterprise.

How Whatfix Enables Modernization Success:

- Accelerates employee proficiency on new core banking systems by delivering in-app guidance and simulation-based learning that shortens the learning curve and minimizes post-launch disruptions.

- Reduces training time, change-management friction, and support costs with self-service help and AI-powered automation that keeps employees productive in the flow of work.

- Ensures compliance and accuracy through guided workflows that standardize complex, high-risk banking processes and reduce manual errors.

- Delivers actionable analytics to measure adoption and ROI, giving leaders real-time insight into system utilization, efficiency gains, and performance improvements.

When modernization initiatives are paired with a digital adoption platform (DAP) like Whatfix, banks don’t just implement new technology, they enable transformation that sticks.

Explore how Whatfix helps banks modernize their core systems, accelerate adoption, and achieve measurable ROI. Request a demo now.